Why So Surprised?

By Twickenham Advisors on March 16, 2018

Markets look a lot less efficient from the banks of the Hudson than from the banks of the Charles.

-Fischer Black

Besides the insurance industry, I cannot think of another industry more driven by statistics than the investment industry. This is ironic because the market is probably the most unpredictable force of nature. Just last year we had the least volatile market in U.S. history! How did this happen now after so many years of market history? Why are we continually so surprised at market moves?

Add more technology, quantitative traders, index funds, and information, and we have still not tamed the wildness of the markets. So, even though every year market returns seem anomalous, we continue to talk about an average return for the markets. Or we find out that a certain style of investing has worked so well in the past, so we must expect that performance to continue in the future.

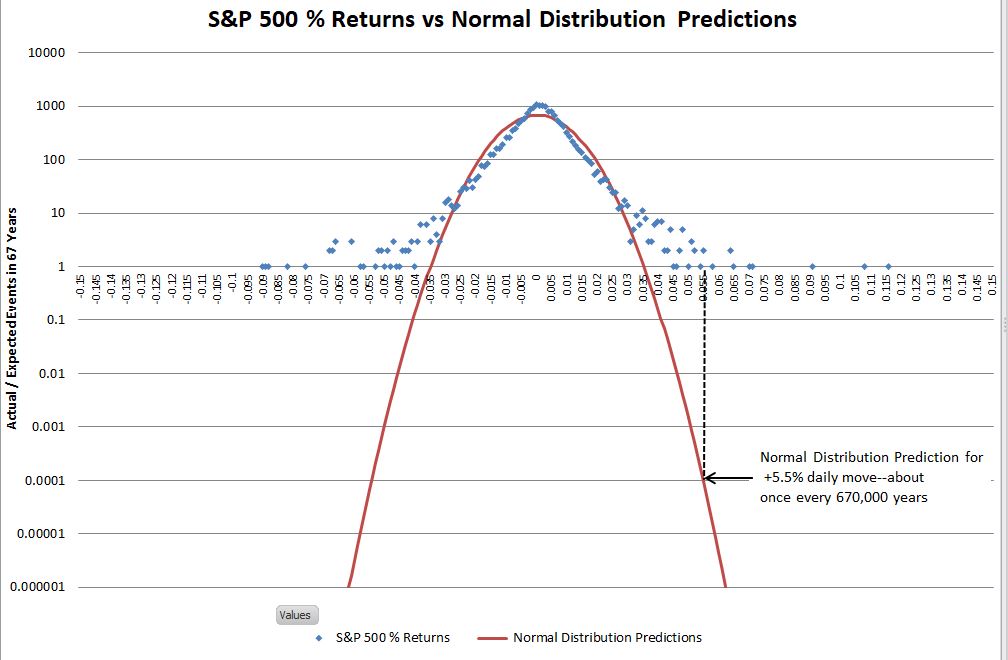

We group a standard deviation of the average return (roughly 68% probability) into a bell curve (a normal distribution) and then are shocked when the market returns something outside of our neat distribution. As you can see in the chart below, market returns are often well outside the probability of what a statistician would predict.

Source: Six Figure Investing

Source: Six Figure Investing

{kind=link}

Instead of one bell curve, the market returns should probably be represented by multiple bells. Mohamed El-Erian (former co-manager with Bill Gross at PIMCO and now the chief economic advisor at Allianz) said, “There is clear evidence that the distribution of potential outcomes from this period of transition is bimodal with relatively high probabilities for both good and bad endpoints.” In other words, stock market returns are often outside what anybody predicts. The below bi-modal distribution of returns is depicted in the graphic below from Allianz Exchange.

The fact is that the market should only surprise us if it acts normal. We must constantly check our premises, as Ayn Rand would say. Is this the same market that our ancestors invested in 100 years ago or even 25 years ago? I would argue that we need to look at the markets through a completely different lens due to dramatic changes in access to information, accounting principle changes, macroeconomic regime changes, trading technologies, technological advances, etc. Even Mr. Old School Warren Buffet points out in his newest letter to shareholders that they should not rely on GAAP earnings as a metric to value Berkshire stock. A blasphemy against our lord and savior Benjamin Graham if I ever heard one!

Considering the recent volatility spikes in February 2018 (volatility, as measured by the CBOE, spiked 3 times higher than the reading throughout 2017), I must say that trying to speculate on something like market moves, volatility, and really anything without yields or interest is more like gambling than investing. Many hedge funds or money managers will show you a backtest of a strategy that works out beautifully. This is dangerous because we never know what will happen to the value of our security when market participants are betting on the price every microsecond. Seeing a strategy (that looks great on paper) perform poorly when the market does something unexpected serves as a reminder to invest in securities with real earnings, revenues, dividends, rents and yields. These dividends are actual returns in your pocket. Every investment has some level of speculation in that there is a probability that the dividends or interest discontinue by the company going out of business or defaulting. But at least we can attribute a more meaningful value to the company with a probability of the sustainability of earnings (or more desirably, growth of those earnings).